![]()

![]()

This is the most difficult part of retirement

planning and the reality is that it all depends on your expenses

and required standard of living at and after retirement.

For many people it comes as a major shock once they realize what

a large capital sum will be required and just how little time

and money they have to implement their retirement plan. As an example, at age 45, you only have another

240 salary payments to fund the required capital that you need

at age 65. Choose Time as your ally right now and he will remain your ally.

The majority of fund members do not truly know and understand the benefits offered by their employee benefit schemes. This is one of the main contributory factors of members not having sufficient capital at retirement. They are under an illusion that their pension or provident fund benefit will be sufficient when they retire.

You

need to understand the benefits you have before you can start

planning for your retirement. Establish if you are a

member of a Defined Contribution (DC) Pension, Defined Benefit

(DB) Pension, Defined Benefit Provident fund or a Retirement

Annuity. You

need to understand the benefits you have before you can start

planning for your retirement. Establish if you are a

member of a Defined Contribution (DC) Pension, Defined Benefit

(DB) Pension, Defined Benefit Provident fund or a Retirement

Annuity. Get the answers to the following questions from your HR or employee benefits administrator: If you do not know what retirement structure is utilized, what

your benefits are and what your monthly contribution is, then

there is no way you can implement an appropriate retirement

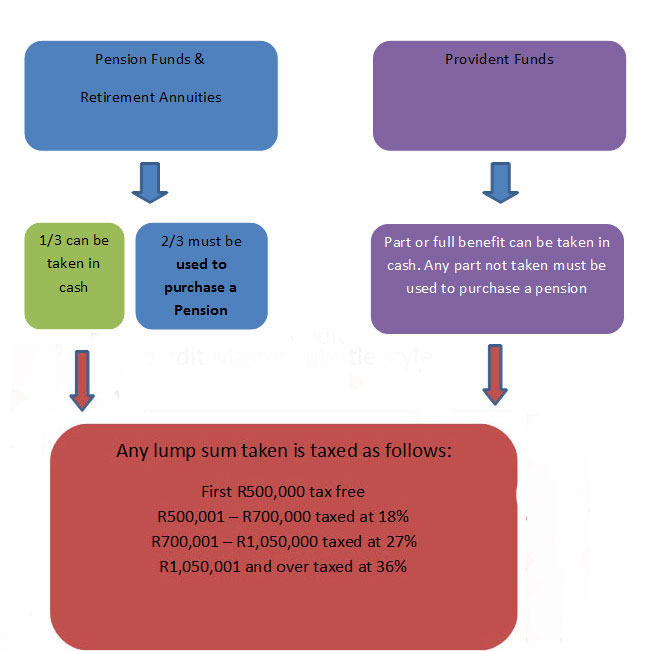

plan. Different rules apply to the availability of capital on retirement from a pension fund, provident fund or retirement annuity. These are explained in the diagram below. The tax implication of the cash lump sum withdrawal will however be the same. It is critical to bear in mind that once the lump sum tax has been deducted (as per the table below) your income tax liability has not been expended. You will remain liable for income tax on the pension/annuity which flows from the portion which is not withdrawn. The pension/annuity will be taxed according the legislated tax tables which also apply to your salary pre-retirement. Although the pension/annuity is taxable it may not ultimately be taxed based on excemptions and rebates granted as per the Income Tax Act.

You will need professional guidance on the most appropriate solution at your retirement and we strongly suggest that you approach a certified financial planner to assist There are two basic choices of annuities,

both have advantages and disadvantages. There are numerous underlying choices available within a life

annuity structure (also known as traditional annuities). The key

features of a guaranteed life annuity are:

Investment-Linked living annuities These products are effectively flexible investment products rather than an annuity, even though the purpose of the product is to produce income. The key features are summarized as follows:

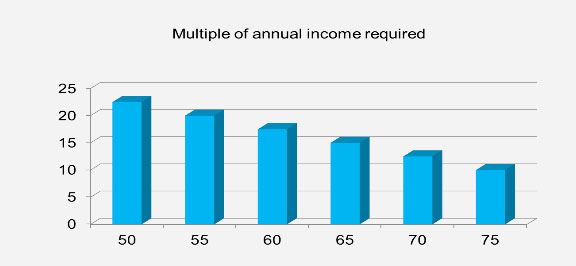

There are numerous factors to consider before deciding on the most appropriate annuity. What makes this decision even more daunting is that once the choice is made there is no turning back, especially when considering the Guaranteed Life Annuity. You make one decision which impacts the rest of your life! When considering the Guaranteed Life Annuity the biggest single factor that determines the annuity rate is the prevailing interest rate. If long-term interest rates are low (as experienced 2009 & 2010) when you buy an annuity, you can expect a lower annuity than if you bought an annuity when interest rates were high. During 2010 you would have thus locked into rates at the bottom of the interest rate cycle should you have invested in a Guaranteed Life Annuity. With the Living Annuity you have the flexibility to determine any required income level as long as you adhere to the legislated minimum and maximum withdrawal rates of 2.5% and 17.5% respectively. Below are guidelines on the appropriate level of income that could be drawn during your retirement lifecycle.

Our service, experience and knowledge extend across the entire spectrum of today’s retirement plans. Whether you are starting a new plan, reviewing the old plan or have a large established retirement program, we can support your needs. Our services include the following:

You are probably already paying fees on your investment portfolio for services that are not been provided and retirement plans not being implemented or reviewed. Is it not time that you demand the services which you are paying for? In this world of uncertainty, independent and objective professional financial advice is imperative. |

We are proudly associated with a number of leading financial services providers including

Financial Tools Click here to get the latest financial tools

|

Investment News Click here to get the lastest financial news

|

Retirement Planning News Click here to get the latest retirement news and newsletters

|

||